If you use a depreciating asset for both business and private purposes, you will need to work out your depreciation deduction based on your business use percentage.

If you use a depreciating asset partly for business purposes and partly for private purposes, you calculate your depreciation deduction based on the business-use percentage (also known as the taxable purpose portion).

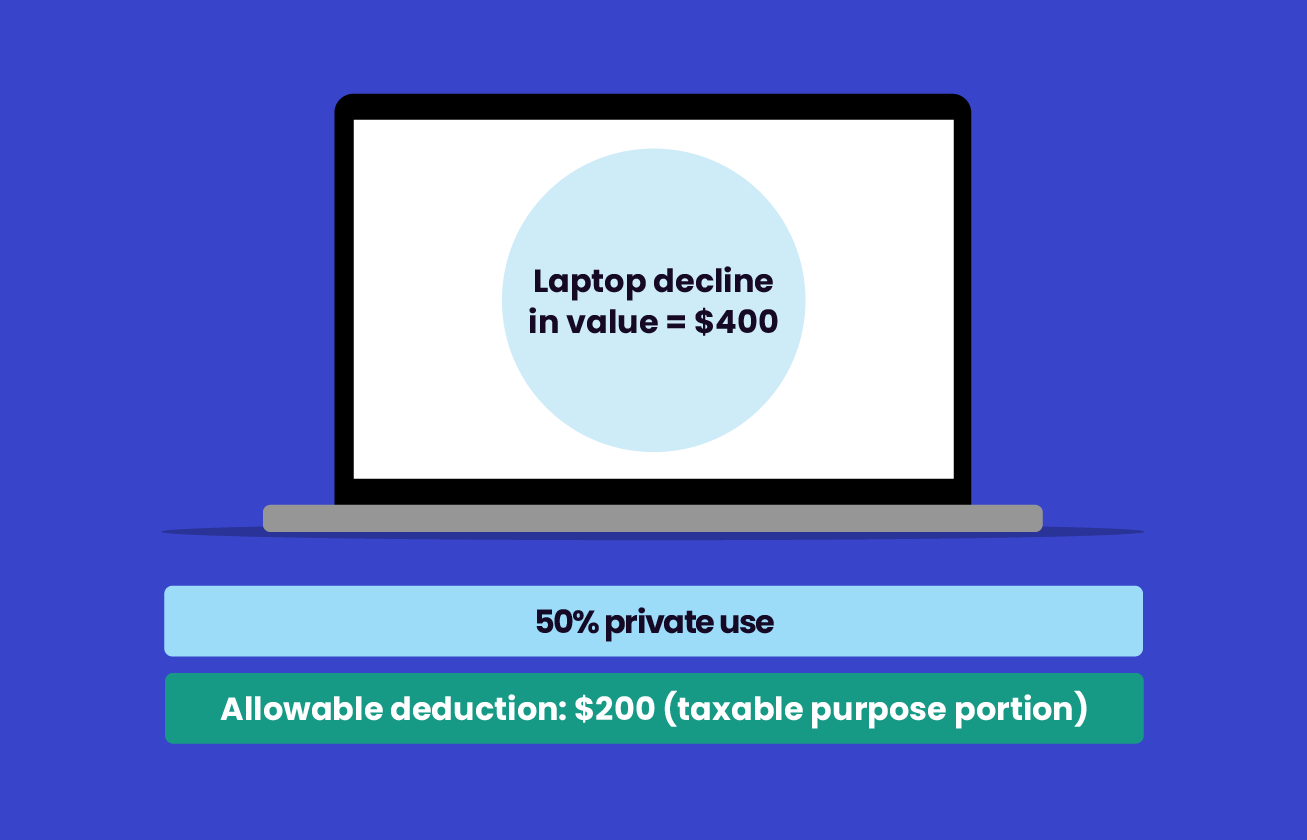

Example

If the decline in value of an asset for an income year is calculated at $400, and the asset is used for business purposes only 50% of the time, you can only claim $200 (50% of $400) as a deduction.

Reviewing asset usage

You must review how much an asset is used for business and other taxable purposes in each of the first 3 income years after the year the asset was added to the small business pool.

If this taxable use proportion changes by more than 10% from your most recent estimate, you must make an adjustment to the opening balance of the small business pool containing the asset to reflect the change in use. You do this before you calculate your small business pool deduction for the year.

If your estimated taxable use percentage changes by more than 10% in later years, you must adjust the opening balance of your small business pool again.

Learn more about how to make an adjustment.